vertigo3d

The sustained downturn in risky assets in 2022 wreaked havoc on a wide range of equities and other financial instruments. One of them is certainly Bitcoin (BTC-USD), which has dropped 64% this year and has destroyed the stock prices of companies that (try to) make a living mining the world’s largest digital currency. I’m not aware of a Bitcoin miner with a higher share price this year, but the downfalls of some have certainly been worse than others.

In what has become the poster child for the downfall of cryptocurrency mining, Scientific Center 🇧🇷NASDAQ: CORZ) filed for bankruptcy protection. Core is the largest cryptocurrency miner by capacity, so theoretically it should have every advantage over competitors. However, too much leverage, combined with a drop in Bitcoin prices, led to its demise and a stock price of less than a penny.

The last time I covered Core, it was the “sell” portion of a Bitcoin miner pairs trade. The stock was priced at $2.02 at the time and has dropped 95% since then. At the time, I observed that Core was heavily leveraged, and the idea was that if there was a prolonged bear market in Bitcoin (it turns out that’s what we got), those with a lot of leverage would suffer the most. Here we are, and Core has now filed for bankruptcy protection.

So what do we do now? Before we look at the Core situation, I want to emphasize that a stock with a market cap of $33 million, a stock price of 9 or 10 cents, and a recent bankruptcy filing is subject to extreme volatility. The very existence of the Core is currently in dispute, as we will see below, and this means that there is a high probability that the current equity value will reach zero, or close to it.

The headline of what I’m about to show is that I don’t think it’s wise to take any positions in this stock given the volatility. If you’re selling Core, you should congratulate yourself, take your profits and move on. On the other hand, I can’t see how this will work for shareholders paying even 10 cents a share. As far as I can tell, Core will actually go out of business if Bitcoin continues to decline or, at best, current equity holders will be so diluted that even 10 cents will look expensive. With all that in mind, I reiterate my suggestion that you think long and hard before doing anything with this action.

I always start my analysis with a chart as I mostly use technical analysis for my own trades. However, with a bankruptcy filing in place, the chart makes no sense. So let’s skip that and jump right into the discussion of funding, as that’s much more relevant in this case.

How did we get here?

The short answer is that Core funded itself as if the good times were never going to end in terms of the Bitcoin price. The company wanted to become the biggest Bitcoin miner and it succeeded. However, the cost of doing this proved to be too much to bear, and we have filed for bankruptcy.

Bitcoin mining economics deteriorated significantly in 2022, which I describe in the article linked above from June. I won’t waste space here to go through this again, but suffice it to say that even though the price of Bitcoin has gone down and down and down, the difficulty of getting Bitcoin has been increasing. This is a very bad combination and has led to Bitcoin miners’ stock prices being decimated.

Core posted an investor update on its bankruptcy filing the week before Christmas, which provides a pretty detailed roadmap of what the company believes will happen going forward.

investor presentation

You can give it a read, but basically, the company filing for bankruptcy is because it can no longer make debt service payments to its creditors. This means that you are in default and need to file for bankruptcy. There has been a lot of miner expansion (financed by debt) in the face of increased difficulty to mine and lower Bitcoin prices. Combine these factors for months on end and you have a failing company.

The company now has a $75 million debtor-in-possession facility, or DIP. Existing holders of convertible notes will turn their debts into equity in the reorganized company, and holders of general unsecured claims will receive common stock and warrants in the reorganized company. What this means is that creditors of various types will receive “significant” portions of the reorganized company’s equity. In practice, this means that the current shareholders will almost certainly be diluted to the point where, even if one of them owns all of Core’s outstanding shares today, that investor would have a small minority stake in the company after the reorganization. Let it sink in.

That’s the risk of buying a company that is in the process of reorganizing; current shareholders will be hugely diluted as the company reorganizes its debt into equity. Management says that the cash generated from operations, as well as the debt-for-equity swaps, should provide enough cash to exit bankruptcy sometime in 2023. But that by no means means that the current share price is any kind of bargain; the company said current investors will be hugely diluted to rid the company’s balance sheet of the unsustainable amount of debt it owes.

Core says, for what it’s worth, that if it were debt-free, its miners would have “significantly” positive cash flow. This implies that if this plan works, Core could theoretically fund its own operations one day. We’ll see, but again, that doesn’t mean current stockholders would see a benefit from exiting bankruptcy proceedings.

Capital structure issues

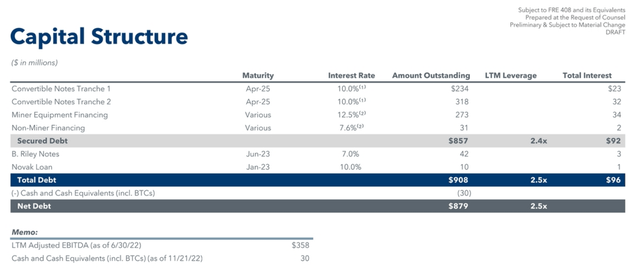

Of course, the company’s filing for bankruptcy meant that its capital structure was, shall we say, suboptimal. Let’s take a look at the updated capital structure from the company’s filing.

investor presentation

There is only $30 million in cash and cash equivalents on the balance sheet and $908 million in debt of various types. One thing for those looking to “haggle” with current equity is that there is $552 million in convertible notes that the company told us will be converted into new equity. The current market cap is $33 million, so you can do the math on what shareholders are likely to have at the end of this. The final amount of equity these convertible note holders receive is up for debate, but it is unlikely to be full face value. Even so, a 50% discount would still be $226 million, or about seven times the current market value. That’s why I was urging extreme caution when trying to buy this stock; people buying today are likely to be left with little or nothing after the restructuring.

For what it’s worth, Core says it won’t be selling any more equipment and will be virtually debt-free after the restructuring. Those things should allow her to operate with the money generated by mining and selling Bitcoins. This argues that the company could somehow survive after the restructuring. That’s good news for employees who want to keep their jobs, but it doesn’t change the outlook for buying the stock today.

As I see it, stock buyers today have two possible outcomes. Either the restructuring doesn’t work and the company goes out of business, or the restructuring works and the shareholders are diluted six or eight or 12 times the current float. The net result for the current stock is about the same in both cases, and that is an extremely low return on the current stock price.

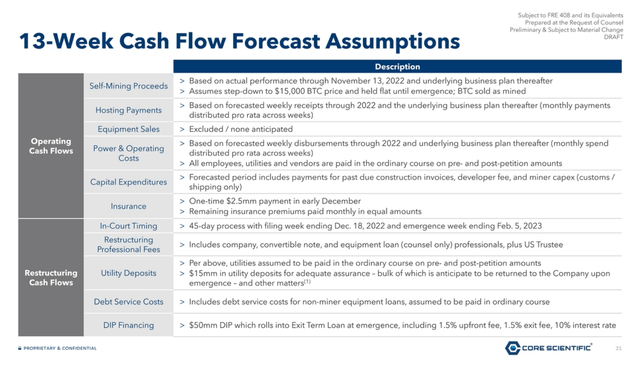

The company provided a useful 13-week cash flow forecast, the assumptions of which you can see below.

investor presentation

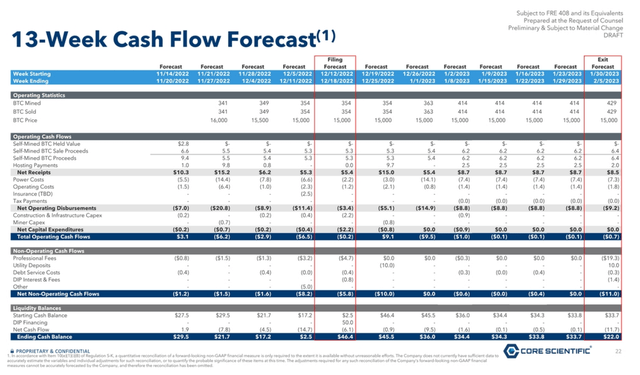

Now, with that in mind, we can look at actual cash inflows and outflows to get an idea of what Core thinks is on the near-term horizon. Apologies for the eye chart; you can click to enlarge it.

investor presentation

The company expects ~$10 million in monthly hosting revenue and ~$25 million in monthly Bitcoin revenue from coins mined and sold. The assumed price is $15,000 per coin, so there are upside and downside risks to this prediction depending on what happens to spot prices.

Importantly, net cash flow is still expected to be negative, which is why Core filed for bankruptcy. Energy and operating costs alone eat up virtually all of your revenue.

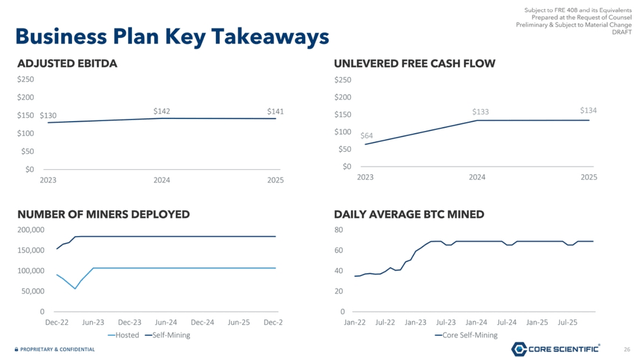

Looking further afield, here’s what Core thinks it can achieve after the restructuring.

investor presentation

He expects something like 65 BTC mined per day, which would equal around $1.1 million of daily revenue. He also expects a fixed number of miners deployed, as well as essentially flat earnings for the foreseeable future. Now, just like the cash flow forecast, these numbers have bullish and bearish BTC spot prices. If the bear market persists and BTC hits $10,000 or so, we will see a huge risk to these numbers. If it goes back to $30k or $40k, Core will do just fine with its reorganized structure. Regardless, keep in mind that the current shareholders will have very little (if any) ownership in any of this under the terms of the restructuring agreement.

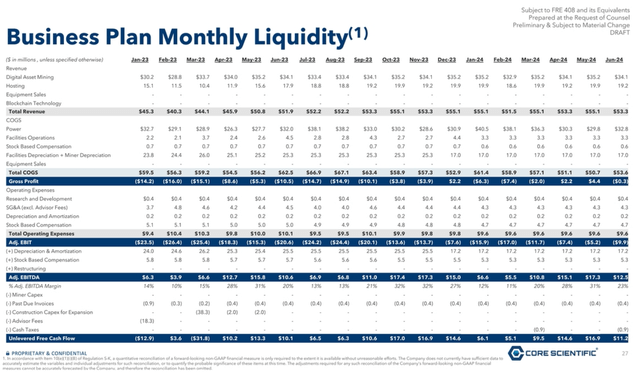

Finally, let’s take a look at the liquidity timeline going forward. Again, click to enlarge or turn to page 34 in the investor presentation to see for yourself.

investor presentation

The bottom line here is that at $16,500 Bitcoin price, Core believes it can survive in terms of sustainable operation going forward. It expects to produce a run rate of $50 million to $55 million in total monthly revenue over the long term, but operating costs will be about the same. I invite those who wish to purchase these shares to also extend the share-based compensation line; the company is predicting ~$5 million a month on SBC going forward indefinitely. Keep in mind that the current market cap is $33 million.

the bottom line

If you’re still with me, it means you’ve seen it loud and clear that I don’t think buying this stock is a good idea. Based on what I see, I believe it is quite likely that this stock will trade very close to zero when the restructuring plan comes to fruition, or potentially before then. I just don’t see a way forward for current stock buyers and I certainly recommend that if you own this for any reason, take the money today, ASAP, and never look back.

I do NOT condone trying to short sell this stock even though I am saying it is likely to lose most or all of its current value. If you could find someone to lend you stock, the costs of doing so and the risk of a short-term squeeze are too great for the reward.

Core has a chance to emerge from this as a company that can truly fund itself going forward. This is particularly true if the spot price of BTC rises significantly. The opposite is also true, if the spot price of BTC drops further, Core could go out of business even after the restructuring.

If you are looking to acquire a share of the new company, I would strongly suggest that you wait until the reorganization is complete and look into purchasing the “new” company. Today’s shoppers will fall by the wayside, according to plan, so I think I’d better stay away.

Editor’s Note: This article covers one or more microcap actions. Be aware of the risks associated with these actions.

Comments

Post a Comment